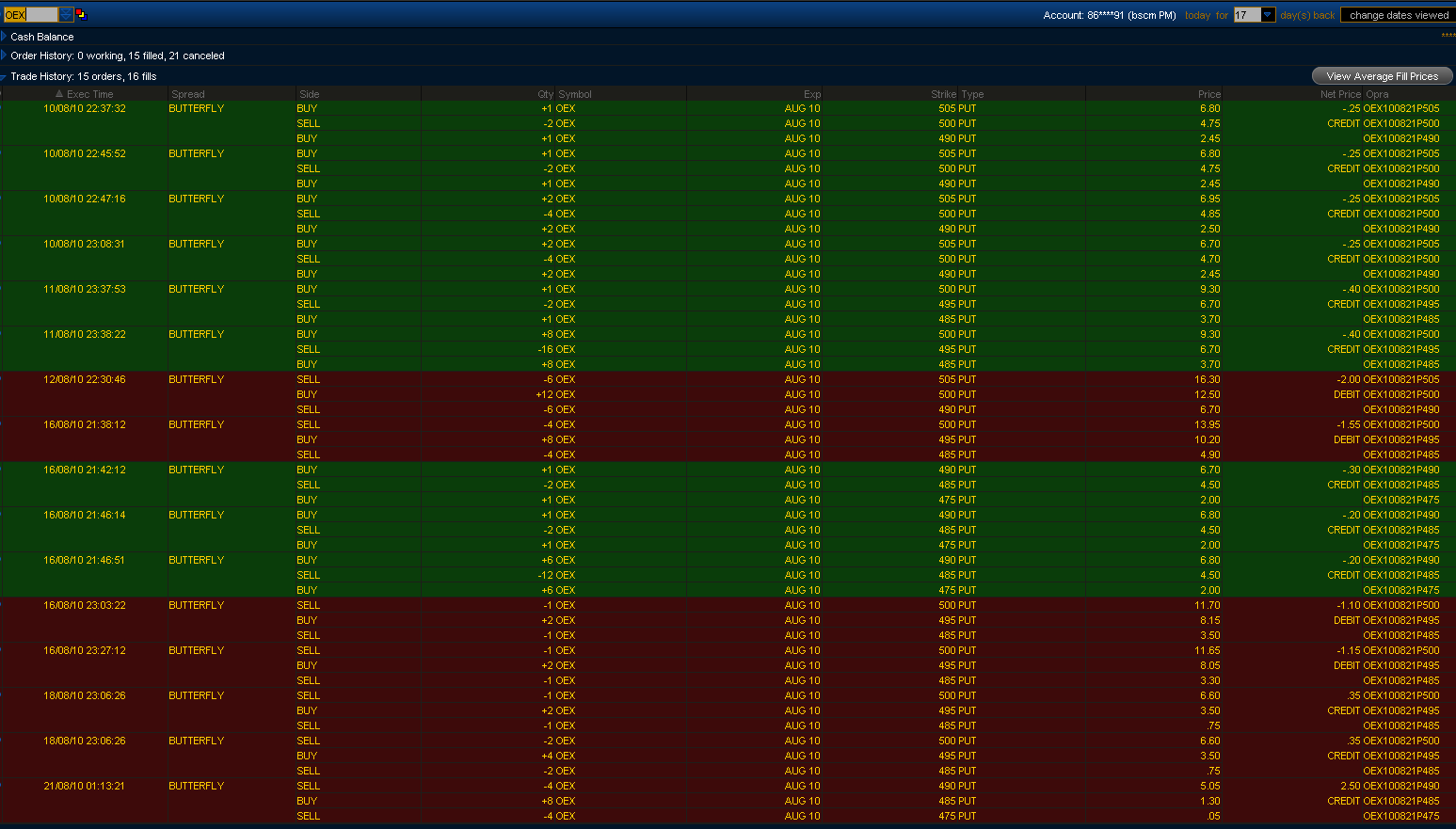

The Good - The only good thing to happen during August was the 2nd lot of hedge trades I had on the OEX Put BWB's for August expiration. If you've been following the blog closely, you will remember that I initially had bought 6 x 505/500/490 Put BWB's (see above) for $0.25 credit. But then after the big down move, I decided to double down and buy some more but at 500/495/485 for $0.40 credit (you can backtest the trades by following the dates and times but note that they are in GMT +8). When the markets failed to bounce I had to get out of the original 505/500/490 BWB's for $2.00 debit (a big loss of $1.75 per contract). Then as the market just kind of went sideways, I thought it was probably a good idea to start peeling off some risk and get out of some of those 500/495/485 BWB's as well by taking some off for $1.55 debit (a further loss of $1.15 per contract) and a couple of other contracts off for $1.10 debit. As I was taking the risk off I bought some more BWB's lower down with the 490/485/475 for $0.25 credit (average). All up I bought 8 contracts. At this point I had 8 of the 490's and about 3 of the 500's left. Now as the markets bounced last Wednesday (see OEX chart below) I was able to take the remaining 500's off for $0.35 credit (profit of $0.75 per contract). At this stage I decided to hold onto the 490's as they were in profit and out of the money but I was expecting some bearish action on Thursday and Friday. Lo and behold, I was right for once and the market moved lower. So on Friday mid morning I took 4 off for $2.50 per contract and decided to let the 4 ride as I didn't think we would have any big moves on Op Ex day and the market internals were holding firm and going sideways. The OEX finished up at $486 resulting in a payout of around $4.00 for the remaining 4 contracts (profit of $4.20). I haven't done the maths yet but when you add up all of those trades I think I might have come out slightly ahead. It was really one of those rare instances when the market cooperates for you and you get the underlying to finish almost dead on your short strike.

The bad - The iron condor on the zb trade for August took a big hit. When the markets tanked, bonds rallied like crazy and as I was short the 131/133 August call spread, you can imagine I took some heavy losses as I was too slow to react. The list of adjustments to my position is as follows:

Notice I started buying OTM call butterflies to move my breakeven higher. However as bonds continued to rally I eventually had no choice but to buy a bunch of the short 131/133 call spreads back and roll my put spreads up as well.

The risk graph now looks like this:

The position has probably made most of it's money right now unless bonds sell off which I think is unlikely. I will probably leave the position on just in case they do decide to pull back a bit. Overall this position has taken off about 5% of my total account in August.

The Ugly - Well the stinker of the month has to be the OTM NDX call butterfly I decided to buy one day before the SPX lost 2.8%. You can see the trade plus the adjustment's below:

This trade was where I lost the other 4% of my account. Say no more.......

No comments:

Post a Comment